a) Explain the difference between short-run equilibrium and long-run equilibrium in monopolistic competition. b) “Perfect competition is a more desirable market form than monopolistic competition.” Discuss.

Wednesday 7 November 2007 Paper 1:

Short Run: When there is a Fixed cost, and only some of the variables chage

Long Run: When there is no fixed cost, all the costs change

(A)

Assumptions

- Large number of firms – each firm has an insignificantly small share of the market.

- Independence – as a result of a large number of firms in the market, each firm is unlikely to affect its rivals to any great extent. In making decisions it does not have to think about how its rivals will react.

- Freedom of entry – any firm can set up business in this market.

- Product differentiation – each firm produces a different product or service from its rivals. Therefore each firm faces a downward sloping demand curve. This is the key difference from perfect competition. Product differentiation involves creating differences between products, either real or imagined, in consumers minds and is likely to involve various forms of non-price competition such as branding and advertising.

Short Run:

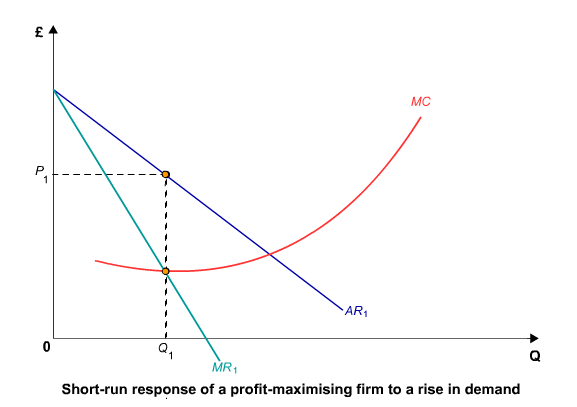

As with other market structures, profits are maximized in monopolistic competition where MC = MR. The AR and MR curves are more elastic than for a monopolist as there are more substitutes available. The profits depend on the strength of demand, the position and elasticity of the demand curve. In the short run therefore firms may be able to make supernormal profits. This situation is shown in the diagram below.

")

Long Run:

In the long run firms will enter the industry attracted by the supernormal profits. This will mean that demand for the product of each firm will fall and the AR (demand curve) will shift to the left. Long run equilibrium occurs where only normal profits are being made as new firms will keep entering as long as there are supernormal profits to be made. In equilibrium, the demand curve (AR) will be tangential to the firm’s long run average cost curve as shown in the diagram below.

The long-run characteristics of a monopolistically competitive market are almost the same as in perfect competition, with the exception of monopolistic competition having heterogeneous products, and that monopolistic competition involves a great deal of non-price competition (based on subtle product differentiation)

")

(B)

- Many buyers and sellers. Nobody has power over the market.

- Perfect knowledge by all parties. Customers are aware of all the products on offer and their prices.

- Firms can sell as much as they want, but only at the price ruling. Thus sellers have no control over market price. They are price takers, not price makers.

- All firms produce the same product, and all products are perfect substitutes for each other, i.e. goods produced are homogenous.

- There is no advertising.

- There is freedom of entry and exit from the market. Sunk costs are few, if any. Firms can, and will come and go as they wish.

- Companies in perfect competition in the long-run are both productively and allocatively efficient.

")

")

{kind=link}